3 month Rules, How to Protect Yourself from Korean Creditors(2026 Inheriting Korea Guide) Renunciation vs. Limited Approval [English Speaking Lawyer. LIBRO]

Introduction: The Second Shock (2026 Inheritance Korea Guide)

Losing a spouse is devastating. But for many foreigners in Korea, the grief is compounded by a sudden shock: Debt Collectors.

In many Western countries, if a person dies, their debt dies with them (or is paid only out of their estate).

In Korea, debt is inherited. If your Korean husband or wife had credit card debt, loans, or unpaid taxes, YOU (and your children) legally inherit that debt and are obligated to pay it back with your own money.

However, the law provides a way out. You have a 3-Month Golden Time to block this debt. This guide explains how. (2026 Inheritance Debt Korea Guide)

1. The “3-Month” Rule: The Deadline You Cannot Miss

Under Article 1019 of the Civil Act, if you do nothing, you are assumed to have accepted Simple Approval (Dan-sun Seung-in).

- Result: You inherit 100% of the assets AND 100% of the debts. If the debt is larger than the assets, you become bankrupt.

The Deadline

You must file a petition to the Family Court within 3 months of the date you learned of the death (usually the date of death). Note: If there are special circumstances (e.g., family living abroad unaware of the death), the court may grant an extension, but this requires a separate application.

⚠️ Critical Warning: Do Not Spend the Money!

Before filing for Renunciation or Limited Approval, do NOT use the deceased’s money (even for living expenses), sell their car, or use their credit card.

Under Article 1026, this act is considered “Implied Acceptance”, and you may lose the right to renounce the debt, even if you file the paperwork later.

2. The Two Shields: Renunciation vs. Limited Approval

You have two legal options to avoid paying the debt with your own money. Choosing the right one is crucial for your family’s safety.

Option A: Inheritance Renunciation (Sang-sok Po-gi)

You declare, “I am not an heir.” You give up everything—assets and debts.

- Pros: Simple procedure. You are 100% free from the debt.

- Cons (The Trap): If you renounce, the debt does not disappear. It moves to the next heir in line.

- Example: If you renounce, the debt goes to your children. If they renounce, it goes to your spouse’s parents, then their siblings. You might accidentally pass a financial bomb to your relatives.

Option B: Limited Approval (Han-jeong Seung-in)

You declare, “I will inherit the debt, but I will only pay it back using the inherited assets.”

- Pros: The debt stops here. It does not pass to relatives. If the deceased had 10M KRW in assets and 100M KRW in debt, you pay 10M, and the remaining 90M is erased. You pay nothing from your own pocket.

- Cons: The procedure is complex. You must liquidate assets and distribute them to creditors strictly according to legal procedures (similar to bankruptcy).

[Table 1] Comparison: Which Should You Choose?

| Feature | Inheritance Renunciation | Limited Approval |

| Concept | “I reject everything.” | “I accept, but liability is limited to the estate.” |

| Effect on Debt | Moves to next-rank kin (Kids/Parents). | Debt ends here (Safest for family). |

| Procedure | Simple court filing. | Complex (Inventory + Liquidation + Publication). |

| Best For… | When you are the last heir or want zero involvement. | When you want to protect children/relatives from debt. |

💡 Lawyer’s Strategy:

The most common strategy is: One person does Limited Approval (to stop the debt chain), and everyone else does Renunciation. However, consult a lawyer to tailor this to your specific family situation.

3. Step 1: Finding the Debt (The “Ansim” Service)

“I don’t know how much debt my spouse had.”

You do not need to guess. The Korean government provides the “Ansim Inheritance One-Stop Service” (An-sim Sang-sok).

- Where: Visit any local Community Center (Dong-jumin-center) or apply via Gov.kr (Government 24).

- What it shows: Banks, Insurance, Loans, Taxes, Pension, and Land ownership.

- Timing: Results arrive via text/online within 7 to 20 days.

- Action: Apply for this immediately after reporting the death to assess whether assets > debts.

4. Step 2: Preparing the Documents

To file a motion with the Family Court, you need specific documents.

Required Documents Checklist

- Deceased:

- Basic Certificate (Gi-bon Jeung-myeong-seo) – Detailed.

- Family Relation Certificate.

- Resident Registration Cancelation (Mal-so-ja Cho-bon).

- You (Heir):

- Alien Registration Card (ARC) or Passport.

- Signature Certificate (issued by your embassy) or Korean Seal Certificate (In-gam) if you have one.

- The Application:

- Petition for Renunciation/Limited Approval.

- Inventory of Assets (for Limited Approval).

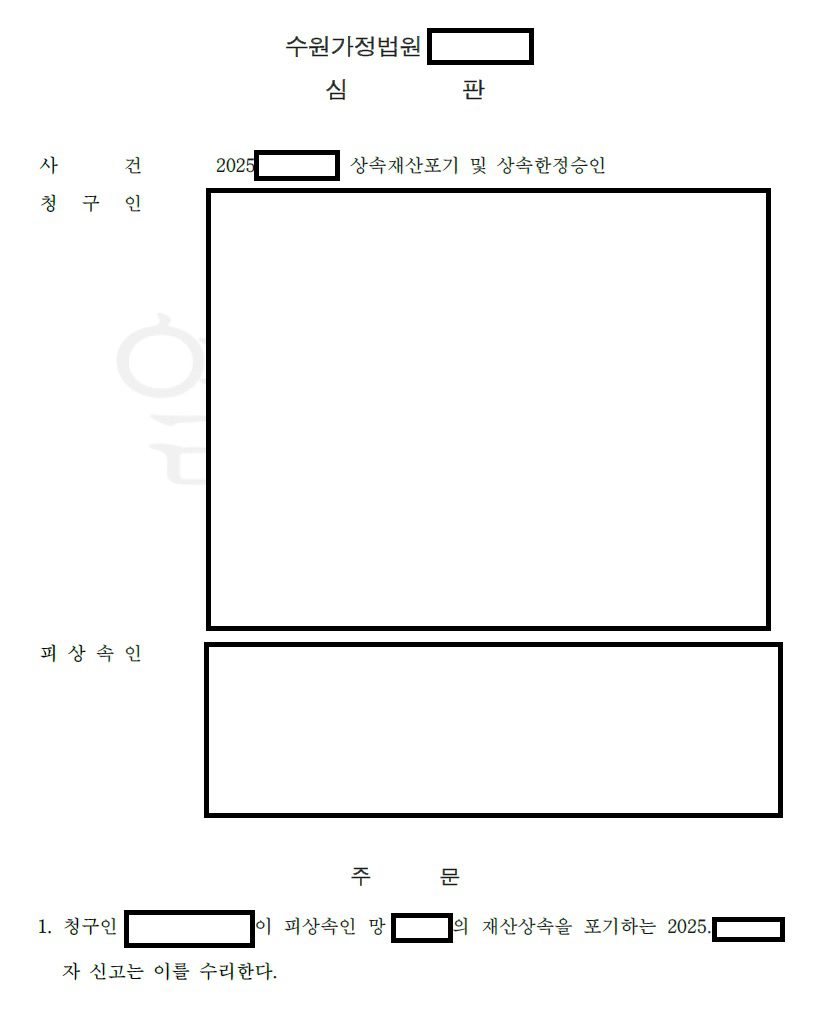

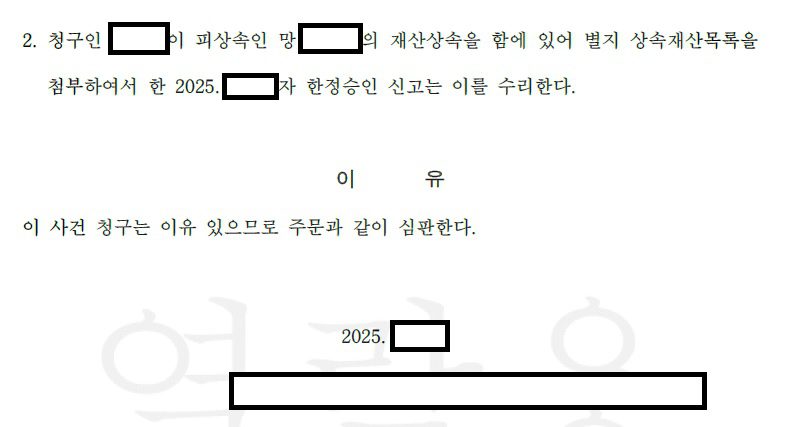

[The provided documents from the Suwon Family Court illustrate two distinct legal measures taken by heirs in 2025 to manage a deceased person’s estate. The first measure involves a court-approved Renunciation of Inheritance (상속재산포기), where the court officially accepted a claimant’s report to give up all rights and liabilities associated with the deceased’s property. The second measure represents a Qualified Acceptance of Inheritance (상속한정승인), a procedure where the court accepted an heir’s report to inherit assets only to the extent of the deceased’s liabilities, supported by an attached list of inherited property. These rulings demonstrate the court’s role in providing legal protections for heirs, allowing them to either fully detach from an estate or limit their debt liability to the value of the inherited assets.]

FAQ: Inheritance & Foreigners

Q1: My children are minors and dual citizens. Do they inherit debt?

A: Yes. Age or nationality does not matter. If you renounce but do not include your children in the petition, the children inherit the full debt. You must act as their legal representative to renounce or limit approval for them.

Q2: Can I collect the Life Insurance money?

A: It depends. If the beneficiary is named as “Heir” or specifically “You,” the insurance money is often considered your property, not the deceased’s estate. This means you might be able to keep the insurance money AND renounce the debt. However, always verify the policy wording with a lawyer before claiming.

Q3: I missed the 3-month deadline. Is it over?

A: Not necessarily. If you genuinely did not know that the debt exceeded the assets (without gross negligence), you can apply for “Special Limited Approval” (Teuk-byeol Han-jeong Seung-in) within 3 months of learning about the excess debt. You must prove you were not negligent.

Q4: I am in my home country. Can I do this remotely?

A: Yes. You do not need to enter Korea. You can grant Power of Attorney (POA) to a Korean lawyer. Note that POA documents usually require Notarization and Apostille (or Consular Legalization) from your home country to be valid in Korean courts.

Summary Checklist

- Stop: Do not spend a single won of the deceased’s money.

- Search: Apply for the “Ansim Inheritance One-Stop Service” at the Jumin-center.

- Decide:

- Assets > Debt? → Simple Approval.

- Debt > Assets? → Limited Approval (Recommended) or Renunciation.

- File: Submit to Family Court within 3 months.

Are you overwhelmed by grief and legal paperwork?

Missing the 3-month deadline can lead to financial ruin.

Once the debt issues are resolved, planning your long-term stability in Korea is the next step. Learn about securing permanent residency here: [Korea Visa Roadmap 2026]

Contact LIBRO Global Client Services. We handle the entire process—from debt tracking to court filing—so you can focus on healing.

Attorney Paul

![[외국인 전문 변호사][ENGLISH SPEAKING KOREAN LAWYER]](https://lawfirmlibro.com/wp-content/uploads/2026/02/Gemini_Generated_Image_fwxnfqfwxnfqfwxn-768x768.jpeg)