[2026 Korea Inheritance Tax Guide] [LIBRO, English Speaking Lawyer]

As a lawyer, I often see expats and overseas Koreans blindsided by Korea’s inheritance tax system. South Korea has one of the highest inheritance tax rates in the world, reaching up to 50%. For “Non-Residents,” the lack of standard deductions can turn a hard-earned family asset into a massive tax bill if not handled correctly.

This guide is your 2026 Roadmap for navigating Korean inheritance law and taxes from abroad. (2026 Korea Inheritance Tax Guide)

- If you want to know about 2026 Inheriting Korea Guide(3 month Rules, How to Protect Yourself from Korean Creditors)

- If you want to know about 2026 Inheriting Korea Guide in Korean([2026 한국 상속 가이드] 한국 상속의 함정: 3개월 안에 빚을 차단하는 법)

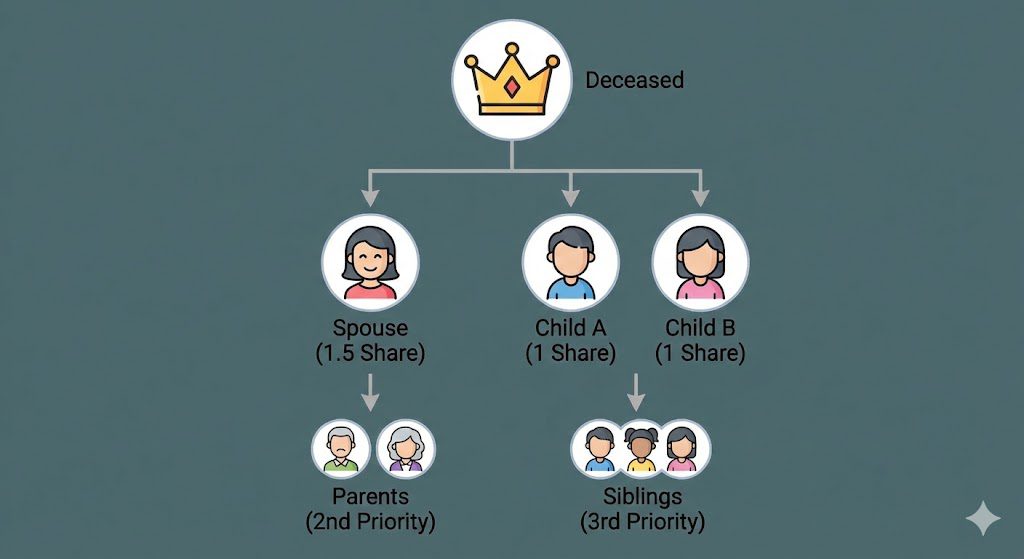

1. Who Inherits? The Legal Order of Succession

Under the Korean Civil Act, the order of inheritance is strictly defined. This order applies regardless of the heir’s nationality.

Legal Inheritance Priority

| Priority | Heirs | Key Note |

| 1st | Direct Descendants (Children, Grandchildren) | Inherit jointly with the spouse. |

| 2nd | Direct Ascendants (Parents, Grandparents) | Only inherit if there are no 1st priority heirs. |

| 3rd | Siblings | Only inherit if there are no 1st or 2nd priority heirs. |

| 4th | Collateral Blood Relatives (Cousins) | Up to the 4th degree; only if no higher heirs exist. |

- The Spouse’s Bonus: The surviving spouse receives a 50% bonus over the shares of children or parents.

- Example Calculation: If there is a spouse and 2 children, the ratio is 1.5 (Spouse) : 1 (Child A) : 1 (Child B). This means the spouse receives 3/7 of the estate, and each child receives 2/7.

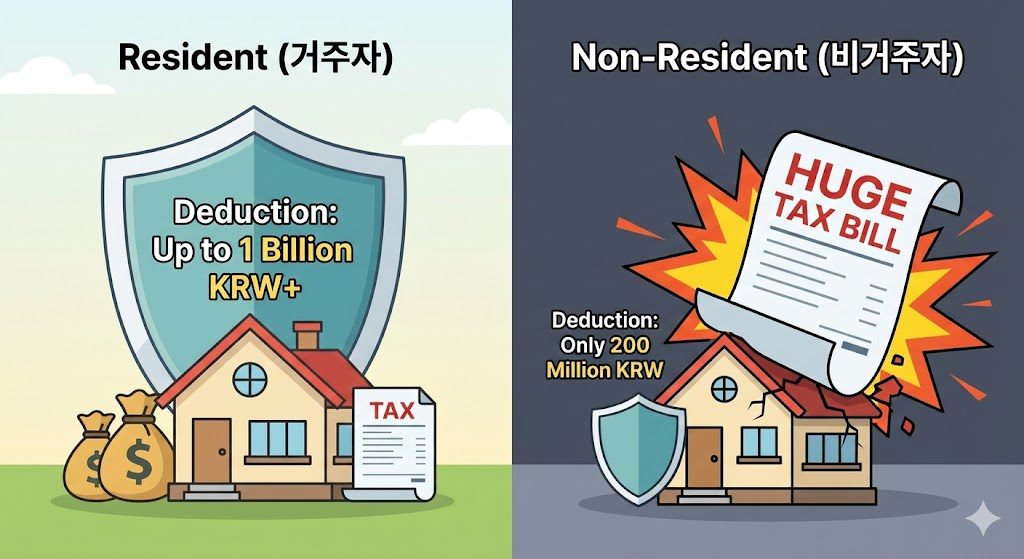

2. The Critical Distinction: Resident vs. Non-Resident

The most important factor in your tax bill is whether the Deceased (the “Pi-sang-sok-in”) was a “Resident” or “Non-Resident” of Korea at the time of death.

- Resident: A person who has a domicile in Korea or has resided in Korea for 183 days or more.

- Non-Resident: Anyone who does not meet the “Resident” criteria.

Why it matters: If the deceased was a Resident, their entire global estate is taxable in Korea, but they get massive deductions (often up to 1 billion KRW or more). If the deceased was a Non-Resident, only their Korean assets are taxable, but they only get a flat 200 million KRW deduction.

3. 2026 Inheritance Tax Rates and Deductions

Tax rates are progressive, meaning the rate increases as the value of the estate grows.

Tax Rate Table

| Taxable Base (After Deductions) | Tax Rate | Progressive Deduction |

| 100 million KRW or less | 10% | – |

| 100m – 500 million KRW | 20% | 10 million KRW |

| 500m – 1 billion KRW | 30% | 60 million KRW |

| 1b – 3 billion KRW | 40% | 160 million KRW |

| Over 3 billion KRW | 50% | 460 million KRW |

The “Deduction Shock” for Non-Residents

- If the Deceased was a Resident: They qualify for the Lump-sum Deduction (500 million KRW) and the Spouse Deduction (minimum 500 million KRW). Essentially, estates under 1 billion KRW are often tax-free.

- If the Deceased was a Non-Resident: They only receive the Basic Deduction of 200 million KRW. They do not qualify for Lump-sum or Spouse deductions.

Example: For a 1 billion KRW apartment inherited from a Non-Resident parent, the taxable base is 800 million KRW (1b – 200m). The tax would be roughly 180 million KRW (800m × 30% – 60m).

4. Mandatory Timeline for Heirs

Missing these deadlines can result in the loss of assets or heavy financial penalties.

- 3 Months (Renunciation/Limited Acceptance): If the deceased had more debt than assets, you must file for “Renunciation” or “Limited Acceptance” at the Korean Family Court within 3 months of learning about the death. (If you want to know more about this, refer to this guide.)

- 9 Months (Tax Filing): If at least one heir or the deceased lives abroad, you have 9 months from the end of the month of death to file and pay inheritance tax (it is 6 months if everyone is in Korea).

- Penalty for Delay: Failure to report on time results in a 20% under-reporting penalty plus daily interest penalties (approx. 10.95% per year).

5. International Document Checklist

Expats can handle the entire process without visiting Korea by granting Power of Attorney (POA) to a Korean lawyer. You will typically need:

- Proof of Identity: Copy of Passport, Signature Notarization, and Apostille (or Consular Authentication).

- Family Documents: Birth certificates or marriage certificates translated into Korean and notarized.

- Power of Attorney: A specific POA for inheritance registration and tax filing, notarized and Apostilled.

- Death Certificate: Original death certificate from the local country, translated and notarized.

6. Frequently Asked Questions (FAQ)

Q: Can I sell the inherited property immediately?

A: Yes, but you must first complete the Inheritance Registration to transfer the title to your name. You will then be liable for Capital Gains Tax (CGT) upon the sale. Note that Non-Residents are not eligible for the 1-house-per-household tax exemption.

Q: What if my siblings and I want to divide the property differently than the law says?

A: You can sign an Inheritance Division Agreement. As long as all legal heirs agree and sign (with notarization/Apostille), you can divide the assets however you wish.

Q: Is there a way to avoid “Double Taxation” between Korea and my home country?

A: While most tax treaties focus on income tax rather than inheritance tax, you may be able to claim a Foreign Tax Credit in your home country for the taxes paid to Korea. This depends on your specific country’s tax laws.

💡 Lawyer’s Insight

“The biggest mistake I see is heirs waiting until they visit Korea to ‘start’ the process. By then, the 3-month debt renunciation window has often closed, or the 9-month tax deadline is looming. Because international documents require Apostilles and translations, the paperwork alone can take over a month. Early intervention is the only way to avoid ‘Penalties’ that can eat up a significant portion of your inheritance”.

Contact LIBRO Global Client Services. [LIBRO] – English Speaking Legal Expert

Attorney Seok Jun Kang