2026 Korea Health Insurance Guide – Navigating Korea Health Insurance (NHI): Costs, Coverage, and Private Options [English Speaking Lawyer. LIBRO]

Introduction: World-Class Care, Complicated Bills

South Korea offers one of the most efficient healthcare systems in the world. As a resident, you have access to top-tier hospitals without waiting months for an appointment.

However, the Korea Health Insurance system (known locally as Guk-min-geon-gang-bo-heom) can be confusing for foreigners.

- Why did I get a bill for 150,000 KRW?

- Do I have to pay if I am a student?

- Does it cover 100% of my surgery?

Whether you are a teacher, a student, or a job seeker, understanding Korea Health Insurance is mandatory for maintaining your visa and your health. This guide breaks down everything you need to know.

1. Is Korea Health Insurance Mandatory?

Yes. Since 2019, the South Korean government has made enrollment mandatory to prevent “free-riding.”

- Who must join: Generally, all registered foreigners (ARC holders) staying in Korea for more than 6 months are automatically enrolled as Regional Subscribers.

- Exceptions:

- Employees: Enrolled immediately upon hiring.

- Students (D-2/D-4): Enrolled upon Alien Registration (ARC issuance) or subject to university-specific policies.

- Penalty: If you do not pay, your visa extension will be denied, and your bank accounts may be seized.

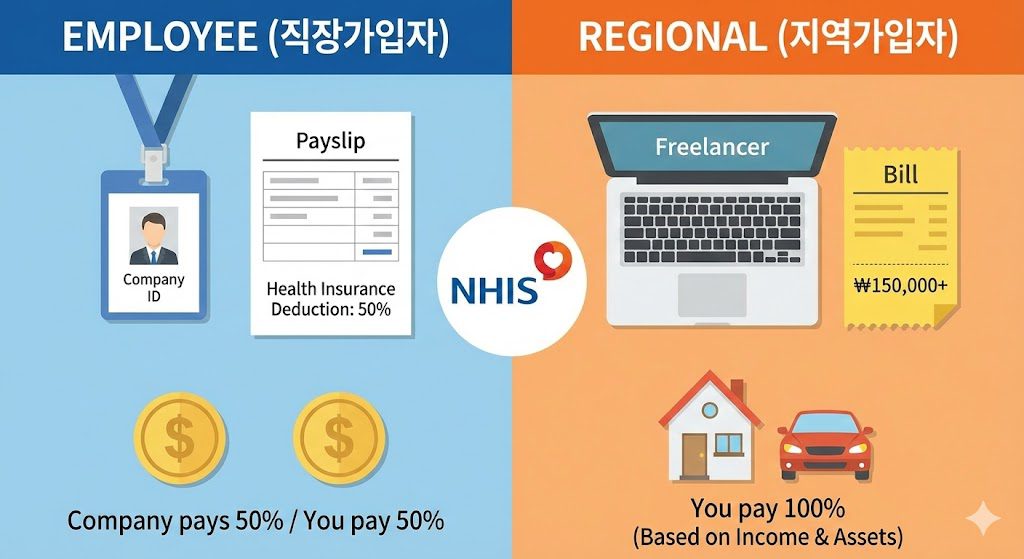

2. Employee vs. Regional: How Much Will You Pay?

Your premium depends entirely on your visa and employment status.

Type A: Employee Subscriber (Jik-jang Ga-ip-ja)

If you work for a company, you are lucky.

- Cost: Approx. 7.19% of your monthly salary (2026 rate).

- The Benefit: You only pay half (approx. 3.6%). Your employer pays the other half.

- Payment: It is automatically deducted from your monthly paycheck (pre-tax).

Type B: Regional Subscriber (Ji-yeok Ga-ip-ja)

If you are a freelancer, job seeker (D-10), or not working, you are a “Regional Subscriber.”

- Cost: Calculated based on your Income + Property (e.g., House Deposit, Car).

- Minimum Premium: Even if you earn $0, you must pay the “Average Monthly Premium.” In practice, many foreigners receive bills around 140,000 ~ 160,000 KRW per month.

- Students (D-2/D-4): International students typically receive a discount (e.g., 50%), bringing the bill to approx. 70,000 ~ 80,000 KRW, though this depends on your school and scholarship status.

⚠️ The D-10 Visa Trap:

Many people switch from a Work Visa (E-7) to a Job Seeker Visa (D-10). When you do this, you lose your “Employee” status (Type A) and become “Regional” (Type B). Your insurance bill will likely jump to the minimum regional rate (~150k KRW). You must budget for this!

3. What Does Korea Health Insurance Cover?

Korea Health Insurance is a cost-sharing system. It does not pay for everything.

[Table 1] Coverage Breakdown

| Service | NHI Pays | You Pay (Copay) |

| Outpatient (Clinic) | 70% | 30% |

| Pharmacy | 70% | 30% |

| Inpatient (Hospital) | 80% | 20% |

| General Checkup | 100% | 0% (Once every 2 years) |

| MRI / CT Scans | Limited* | 100% (Unless for cancer/brain disease) |

| Dental (Scaling) | 70% | 30% (Once a year) |

| Plastic Surgery | 0% | 100% (Cosmetic purposes) |

- Key Takeaway: For serious illnesses, NHI is a lifesaver. However, coverage for advanced scans (MRI) is strictly limited to medical necessity. For minor injuries, you often pay 100%.

4. Filling the Gap: “Sylbi” (Private Insurance)

Because Korea Health Insurance leaves you with a 20-30% bill, most residents purchase private supplemental insurance called “Sylbi” (Sil-son Ui-ryo-bi).

- What it does: It reimburses a portion of the Copay (the 20-30% you paid). Note: Newer plans (4th Generation) may have higher deductibles for non-covered treatments like manual therapy.

- Cost: Varies by age.

- 20s-30s: ~10,000 – 20,000 KRW/month.

- 40s+: ~30,000 – 50,000 KRW+/month.

- How to Claim: You pay the hospital first, take a photo of the receipt, upload it to the insurance app, and get the money back.

💡 Pro Tip: Relying only on NHI is risky. NHI + Sylbi is the standard safety net in Korea.

5. Adding Your Family (Dependents)

If you are an Employee Subscriber, you can register your non-working family (Spouse, Children, Parents) as Dependents (Pi-bu-yang-ja).

- The Perk: They pay 0 KRW. They are covered under your premium.

- Conditions:

- Income/Property Limit: They must have income below a certain threshold (e.g., 20M KRW/year) and limited assets.

- Residency Rule: Generally, foreign dependents must have lived in Korea for 6 months to be eligible.

- Exceptions: Spouses (F-6), minor children (under 19), and certain visa holders (D-2, E-9, F-5) may be exempt from the 6-month wait.

- Documents: Family Relations Certificate (Apostilled/Translated) + ARCs.

Note: Regional Subscribers (Type B) cannot add dependents for free. The premium is calculated based on the household’s total income/assets.

6. FAQ: Managing Your Insurance

Q1: I am leaving Korea for a vacation (over 1 month). Do I still pay?

A: You can apply for a “Suspension of Payment” if you are gone for more than 1 month.

- Important: Do not assume this is automatic. You must call NHIS (1577-1000) or visit a branch to apply for the suspension before you leave. If you don’t, you will be billed.

Q2: I received a text about unpaid premiums. Will I be deported?

A: You won’t be deported immediately, but you will face Visa Restrictions. The Immigration Office checks your tax and insurance payment history. If you have arrears, they will limit your visa extension to only 6 months or reject it entirely.

Q3: Can I opt out of Korea Health Insurance?

A: Only in very specific cases (e.g., A-1 Diplomats, or if you have foreign company insurance that provides equal or better coverage than NHI). The burden of proof is high, and exemptions are rarely granted to regular residents.

Summary Checklist

- Identify Status: Are you an Employee (50% off) or Regional (Full pay)?

- Budget Correctly: Prepare ~150,000 KRW/month if you are switching to a D-10 visa.

- Get Private Insurance: Sign up for “Sylbi” to cover the gaps in Korea Health Insurance.

- Register Family: If you have a job, bring your eligible family under your plan as dependents.

- Pay on Time: Use Auto-Debit to ensure your visa renewal goes smoothly.

Need Help with Dependent Registration or Claims?

Navigating the NHIS system with foreign documents can be difficult.

Contact LIBRO Global Client Services for assistance with document translation, Apostille verification, and resolving insurance disputes.

[Request NHIS Support]

Attorney Seok Jun Kang