2026 Korea Medical Insurance Guide – “Hospital Bills are Cheap?” Only If You Have This! (The Ultimate Guide to Korean National Health Insurance) [English Speaking Lawyer. LIBRO]

Introduction: World-Class Healthcare at a Cost (2026 Korea Medical Insurance Guide)

One of the best things about living in Korea is the healthcare system. It is fast, high-quality, and accessible. You can walk into a specialist’s clinic without an appointment and see a doctor in 10 minutes.

However, many foreigners are shocked when they receive a yellow bill in the mail from the NHIS (National Health Insurance Service) asking for over 150,000 KRW every month.

- “Is this mandatory?”

- “Why is it so expensive?”

- “Does it cover everything?”

This guide explains the Mandatory Enrollment Rule, how to calculate your cost, and the secret weapon called “Sylbi” that covers what NHI doesn’t.

1. What is NHI (National Health Insurance)?

Korea operates a single-payer system called NHI (Guk-min-geon-gang-bo-heom).

- Concept: Everyone pays a monthly premium, and the government pays about 60~80% of your medical bills. You pay the remaining 20~40% (Copayment).

- Mandatory: Generally, any foreigner staying in Korea for more than 6 months (or immediately for certain visas like D-2, E-7) is automatically enrolled as a Regional Subscriber if not employed. Note: Some exceptions apply for A-visas or short-term stays..

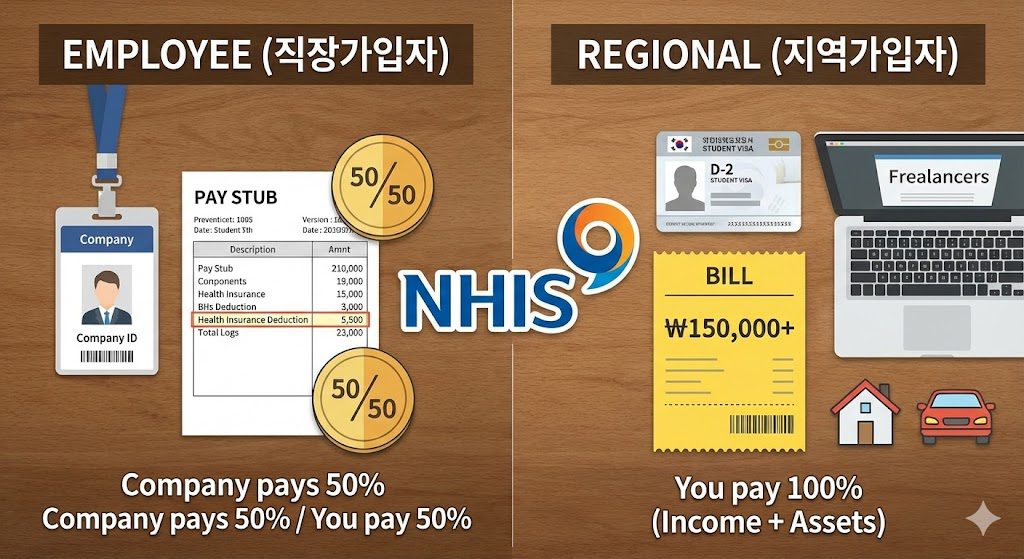

2. Employee vs. Regional: Which One Are You?

Your insurance status depends entirely on your job.

Type A: Employee Subscriber (Jik-jang Ga-ip-ja)

- Who: E-7, E-2, F-visas working full-time at a company.

- Cost: Approx. 7.09% of your monthly salary (rate adjusted annually).

- Good News: You only pay half (approx. 3.5%). Your company pays the other half.

- Payment: Deducted automatically from your paycheck (pre-tax).

- Activation: The company HR handles everything on your first day.

Type B: Regional Subscriber (Ji-yeok Ga-ip-ja)

- Who: Students (D-2), Job Seekers (D-10), Freelancers, F-series visas without a full-time job.

- Cost: Calculated based on your Income + Property (Deposit/Car).

- Minimum Premium: Even if you have 0 income, you are charged the “Average Monthly Premium.” In practice, many foreigners receive bills around 140,000 ~ 160,000 KRW per month.

- Student Discount: D-2 and D-4 students often receive a discount (e.g., 50%), bringing the bill to 70,000~80,000 KRW, but this depends on university policies and government subsidies.

⚠️ Warning for D-10 (Job Seekers):

When you quit your job and switch to D-10, you lose your “Employee” status and become a “Regional” subscriber. Your premium will likely jump to the minimum regional average (150k+). You must pay this to maintain your visa status.

3. Coverage: What Do You Get?

[Table 1] What NHI Covers vs. You Pay

| Service | NHI Pays | You Pay (Copay) | Approx. Cost to You |

| Clinic Visit (Cold/Flu) | 70% | 30% | 4,000 ~ 6,000 KRW |

| Pharmacy (Prescription) | 70% | 30% | 3,000 ~ 5,000 KRW |

| Hospitalization (Inpatient) | 80% | 20% | Varies |

| General Checkup | 100% | 0% | Free (Once every 2 years) |

| MRI / Ultrasound | Limited* | 100% (mostly) | Expensive (Unless critical) |

| Dental (Scaling) | 70% | 30% | ~15,000 KRW (Once a year) |

- Note on MRI/CT: NHI coverage for expensive scans like MRI is strictly limited to serious conditions (cancer, brain disease). For minor injuries, you often pay 100%.

4. The Secret Weapon: “Sylbi” (Private Insurance)

NHI is great, but it leaves a gap. If you break a leg and need surgery + MRI + Hospitalization, your 20~30% copay can still be millions of won.

This is why almost all Koreans have “Sylbi” (Sil-son Ui-ryo-bi).

What is Sylbi?

It is private insurance that reimburses the Copay (the 20-30% you paid).

- Cost: Dependent on age and plan.

- 20s: Approx. 10,000 ~ 20,000 KRW.

- 40s+: Approx. 30,000 ~ 50,000 KRW+.

- Benefit: It covers non-NHI items like MRIs and special injections (subject to policy limits).

- How to get it: You must contact a private insurance agent (Samsung Fire, Hyundai Marine, Meritz, etc.).

💡 Recommendation: Do not rely on NHI alone. NHI + Sylbi is the standard combination for financial safety in Korea.

5. Family: How to Register “Dependents” (Pi-bu-yang-ja)

If you are an Employee Subscriber (Type A), you can register your non-working spouse and children as Dependents.

- Benefit: They pay 0 KRW. They are covered under your premium.

- Conditions:

- Income/Property Limit: They must meet strict income and property asset limits (not just “zero income”).

- Residency: Generally, foreign dependents must have lived in Korea for 6 months to be eligible (Spouses and minor children may be exempt from this waiting period).

- Documents:

- Application Form.

- Family Relations Certificate (must be Apostilled/Verified and Translated).

- Alien Registration Cards (ARC) of all family members.

Note: Regional Subscribers (Type B) cannot add dependents for free. The premium is calculated based on the household’s total income/assets.

6. FAQ: Common Foreigner Mistakes

Q1: I am leaving Korea for a month. Do I still pay?

A: If you leave for more than 1 month, you may apply for a “Suspension of Payment.” Do not assume this happens automatically. You should visit or call the NHIS branch to confirm your suspension status before leaving to avoid accumulating arrears.

Q2: I ignored the bills. What happens?

A:

- Bank Seizure: They can freeze your Korean bank account.

- Visa Denial: You cannot extend your visa or change visa types until you pay all arrears.

- No Insurance: Your coverage stops immediately, and you pay 100% at hospitals.

Q3: Can I opt-out?

A: Generally, No. Exceptions exist only for:

- Diplomats (A-1).

- Foreigners covered by foreign company insurance that guarantees better coverage than NHI (Requires strict proof and approval from NHIS).

Q4: How do I pay the Regional bill?

A: The bill arrives by mail. To avoid missing payments (and visa issues), set up Auto-Debit (Ja-dong I-che) by calling 1577-1000 (English Service available) or visiting the NHIS branch.

Summary Checklist

- Check Status: Are you Employee (Company pays half) or Regional (You pay all)?

- Budget: If Regional, expect a bill around ~150,000 KRW/month.

- Get Sylbi: Sign up for private medical indemnity insurance to cover the 30% copay.

- Register Family: If employed, register eligible family members as dependents to save money.

- Leaving Korea? Call NHIS to apply for payment suspension if gone for >1 month.

Confused by the NHIS Bill or Family Registration?

Registering overseas family members as dependents requires complex Apostilled documents.

[Request NHIS Assistance]

Attorney Seok Jun Kang